1-taka insurance!

News desk: Insurance is no longer just about expensive yearly plans. A growing shift in the digital insurance industry is making coverage simpler, cheaper and more accessible for everyday users. Products like ‘1-taka’ or “1-rupee” trip insurance are at the center of this transformation, offering a practical entry point for many first-time customers.

Traditionally, insurers focused on selling high-value annual policies, a model that often created resistance in price-sensitive markets. Many consumers viewed insurance as an unnecessary expense rather than a useful financial tool. That perception is now changing with the rise of micro-insurance- low-cost, easy-to-understand products designed around everyday needs. These policies are simple, relevant and quick to adopt, making them especially appealing to digital-first users.

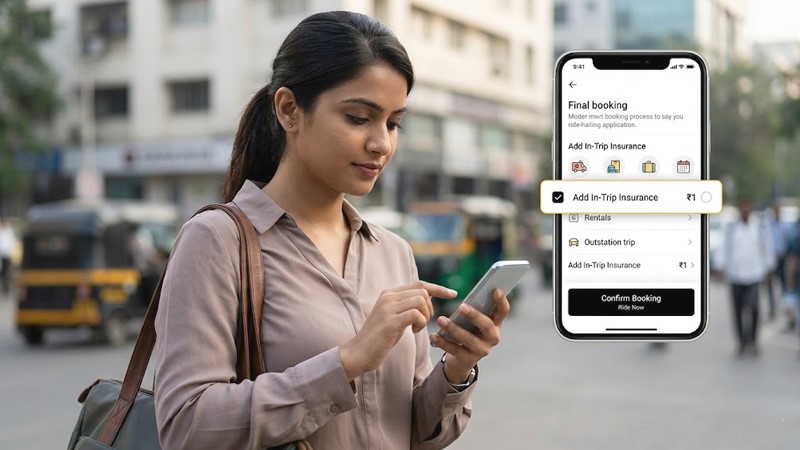

A clear example of this shift can be seen in the strategy adopted by Indian digital insurer Acko. In partnership with ride-hailing platform Ola, the company embedded insurance directly into the ride-booking process, allowing users to add coverage seamlessly. The pricing model was tailored to different travel types: 1 rupee for in-city trips, 10 rupees for Ola Rentals and 15 rupees for Ola Outstation journeys. By aligning pricing with real usage patterns, the product became both practical and highly relevant to users.

Despite its minimal cost, the insurance offered meaningful protection. The 1-rupee in-trip cover provided benefits of up to 500,000 rupees, covering accident-related medical expenses, loss of baggage or laptops, missed flight compensation, ambulance services and emergency hotel stays. This combination of affordability and real-world value has helped redefine how consumers perceive insurance, demonstrating that it can be both accessible and genuinely useful in everyday situations.

Equally important to its success was the simplicity of the user experience. The insurance option was fully integrated into the ride-booking journey, enabling users to opt in with a single click, without paperwork or lengthy forms. The claims process was also streamlined; users could submit claims within approximately two minutes through the app, with most cases resolved within 48 to 72 hours. This level of speed and convenience has played a key role in building user trust.

Adoption figures further highlight the impact of this approach. Within the first nine months of launch, more than 250 million policies were sold, according to industry data. The attach rate exceeded 50 percent, meaning that more than half of all rides included the insurance option. The platform also maintained a technical uptime of 99.99 percent, reflecting the reliability of the underlying digital infrastructure.

Beyond pricing and product design, distribution has been a critical driver of success. Unlike traditional insurers that rely on agents or physical channels, Acko leveraged platform partnerships to reach users within their everyday digital activities. This removed the need for separate customer acquisition efforts, as insurance became a natural extension of the user journey. The company has expanded this model beyond Ola to platforms such as RedBus, Zomato, GoIbibo and Dunzo, demonstrating the scalability of this approach.

This strategy reflects the broader rise of embedded insurance, where coverage is integrated into services that people already use. Instead of requiring users to actively seek out insurance, it is offered at the point of need, making it easier to understand and adopt. This not only improves the customer experience but also reduces acquisition costs while enabling rapid growth.

The implications of this model extend beyond India and are particularly relevant for emerging markets such as Bangladesh, where insurance penetration remains low. In many cases, consumers still view insurance as a luxury rather than a necessity. However, the rapid expansion of digital platforms, including ride-sharing, mobile financial services, e-commerce and online ticketing, makes a strong opportunity to introduce embedded micro-insurance products. By integrating low-cost coverage into these services, insurers can reach a wider audience and build trust more effectively.

.jpg)

.jpg)