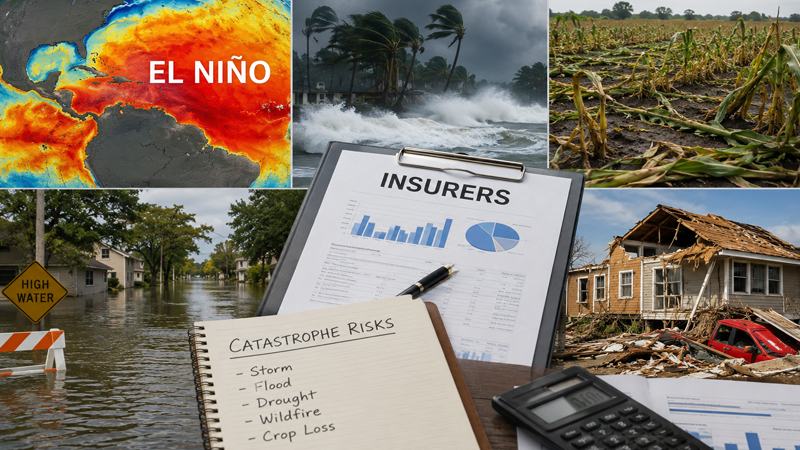

Rising El Niño Odds Urge Insurers to Prepare for Global Storm, Crop and Catastrophe Risks

Staff Correspondent: The probability of a significant El Niño developing in the equatorial Pacific has increased markedly, with forecasters assigning an 82 percent chance of emergence between May and July 2026 and a 96 percent likelihood that the pattern will persist through the Northern Hemisphere winter of 2026–27. The U.S. Climate Prediction Center further estimates roughly a two-in-three chance of the event reaching strong or very strong intensity at its peak, prompting insurers and reinsurers worldwide to reassess exposure across property, agriculture, marine, and specialty lines as correlated weather extremes threaten to drive up claims and reshape risk pricing.

This evolving climate situation arrives against a backdrop of already elevated global temperatures, amplifying concerns for the insurance industry. Warmer sea surface temperatures, weakening trade winds, and subsurface heat anomalies are accelerating the transition, with models indicating potential for impacts that could rival or exceed the 2015–16 event. Underwriters are now scrutinizing catastrophe models more closely, as El Niño’s teleconnections create simultaneous stresses across distant regions, increasing the risk of accumulated losses that challenge diversification assumptions.

In terms of property and casualty exposure, the pattern typically suppresses Atlantic hurricane activity through higher wind shear, offering some relief to heavily insured coastal markets in the United States, Caribbean, and Gulf of Mexico. However, this benefit is offset by elevated risks elsewhere, including heightened eastern Pacific tropical cyclone activity that could impact Mexico, Central America, and Hawaii, as well as increased inland flooding from heavier rainfall in parts of the southern and southwestern United States. Insurers in flood-prone areas such as Florida, California, Texas, and the Southeast are particularly attentive, with analysts warning that additional rainfall and storm threats could exacerbate existing coverage gaps, push reinsurance costs higher, and contribute to further premium hardening or withdrawal of capacity in vulnerable zones.

Agricultural insurance faces some of the most direct pressures. Drier conditions and weakened monsoons in Southeast Asia, Australia, India, and parts of southern Africa could reduce yields of key crops such as rice, wheat, cocoa, coffee, and palm oil, while flooding in the eastern Pacific and South America threatens harvests and infrastructure. These shifts raise the prospect of widespread claims under crop insurance and parametric products, potentially tightening global commodity supplies and driving food price volatility that indirectly affects business interruption and supply chain policies. Reinsurers, already managing elevated natural catastrophe budgets, are monitoring these correlated agricultural and weather risks closely, as simultaneous events across multiple continents could test aggregate limits and capital reserves.

Broader implications extend to wildfire, drought, and heat-related covers, with heightened wildfire potential in drier regions and increased demand for parametric solutions that provide rapid payouts based on indexed triggers rather than traditional loss adjustment. Industry observers note that a strong El Niño could accelerate repricing of catastrophe risk, influence renewals, and encourage greater adoption of resilience measures and climate-linked underwriting adjustments. While Q1 2026 saw relatively contained insured catastrophe losses, the second half of the year and into 2027 may see a reversal if the forecasted extremes materialize, particularly when layered atop ongoing challenges from climate change.

Experts caution that while probabilities strongly favor development, the precise strength and regional manifestations carry uncertainty, leaving room for outcomes that vary from moderate to extreme. Insurers are urged to enhance scenario modeling, diversify portfolios, refine pricing to reflect shifting hazards, and collaborate with clients on mitigation strategies such as improved flood defenses, drought-resistant agriculture, and expanded parametric coverage. As monitoring intensifies through the Northern Hemisphere summer, regular updates from NOAA, the World Meteorological Organization, and specialized risk consultancies will play a pivotal role in helping the sector navigate what could emerge as one of the more consequential climate influences on insurance markets in the latter half of the decade.

.jpg)

.jpg)